Suppressor Financing: The Affordable Path to Your First Can

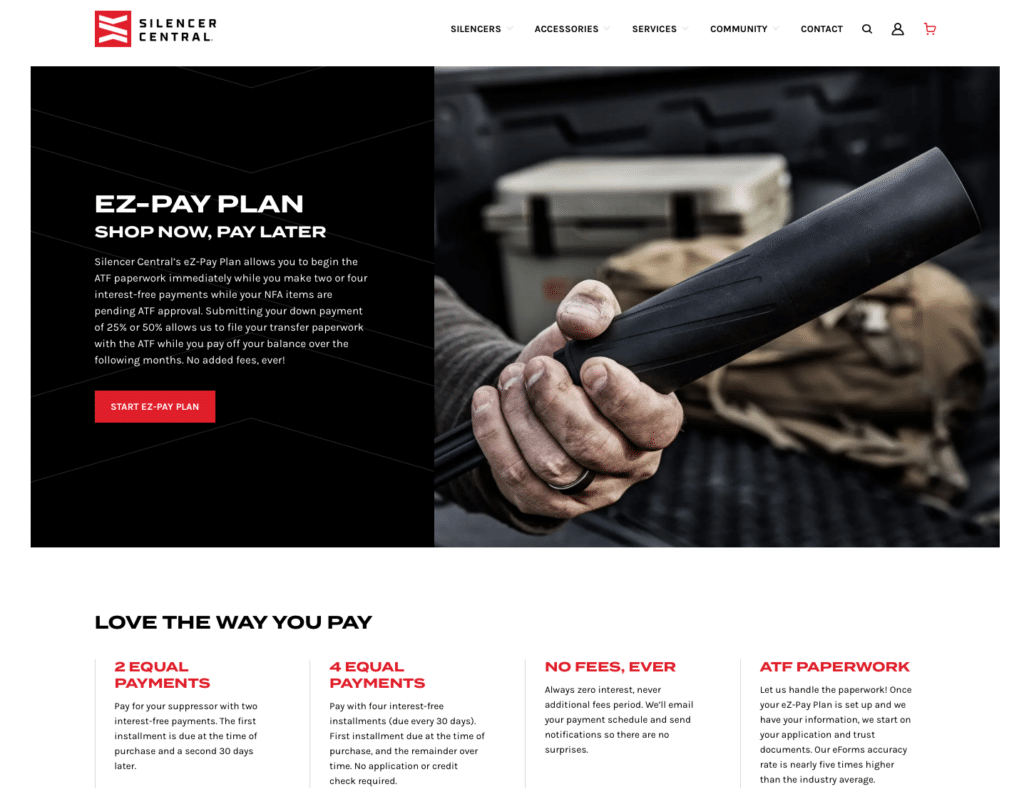

Silencer Central's EZ Pay lets you split suppressor payments into monthly installments while your ATF paperwork processes.

Last updated: June 6, 2026 · Originally published: March 8, 2026

In This Article

- Suppressor Financing Options: How to Buy a Suppressor Without Paying All at Once

- Why Suppressor Financing Is Different from Standard Firearms Financing

- Suppressor financing: Silencer Central’s Payment Program

- Suppressor financing: Local Dealer Layaway and Payment Plans

- Suppressor financing: Consumer Financing Through Credit Cards and Personal Loans

- Suppressor financing: The $0 Tax Stamp and What It Means for Financing in 2026

- Suppressor financing: NFA-Specific Financing Considerations

- How to Evaluate Suppressor Financing Offers

- Suppressor financing: Budgeting Realistically for Your First Suppressor in 2026

- Frequently Asked Questions About Suppressor Financing

Suppressor Financing Options: How to Buy a Suppressor Without Paying All at Once

Suppressor financing has become one of the most accessible ways to enter NFA ownership in 2026, with multiple options available that let buyers spread the cost of a suppressor over months while the ATF Form 4 is processed — effectively turning the wait time into a payment window. Quality suppressors range from approximately $400 for entry-level rimfire models to $1,500 and above for premium centerfire designs, and the elimination of the $200 federal tax stamp effective January 1, 2026, has already reduced the total acquisition cost. For buyers who want to own a quality suppressor without a large upfront payment, understanding the financing landscape is the first step.

This guide covers every financing option available to suppressor buyers in 2026: Silencer Central’s installment program, dealer payment plans, credit and consumer financing options, how the NFA transfer process interacts with financing, and what to watch for in financing terms specific to NFA items. Whether you are budgeting for your first suppressor or adding to an existing collection, knowing your payment options makes the decision easier.

Key Takeaways

- Many Class III dealers offer layaway or payment plans during the Form 4 wait period (typically 30–90 days)

- Silencer Central offers financing through their online purchase process — apply at checkout

- Personal loans or 0% APR credit card promotions can make suppressor financing interest-free

- Since the $200 tax stamp was eliminated January 1, 2026, the total cost is now just the suppressor price plus dealer transfer fee

- Some dealers allow you to pay off the suppressor before Form 4 approval — you’ve already paid when it’s time to pick up

Why Suppressor Financing Is Different from Standard Firearms Financing

NFA item purchases have a structural characteristic that makes them distinct from standard firearms financing: you pay for the suppressor before you receive it, and the delay between purchase and possession is determined by ATF Form 4 processing time — which in 2026 ranges from single-digit to low double-digit days for eForm 4 submissions. This means the financing window overlaps with the ATF wait period rather than beginning after delivery, which is actually a practical advantage for buyers who use a payment plan. The Form 4 is submitted after purchase, and in many financing arrangements, buyers can make several installment payments before ATF approval arrives and the suppressor ships. For buyers who can apply monthly installment payments toward a suppressor during the approval window, the total out-of-pocket at the time of possession may be substantially reduced from the day-of-purchase total. Understanding this timeline helps structure the most effective financing approach for your situation.

Suppressor financing: Silencer Central’s Payment Program

Silencer Central, the anchor sponsor of the Silencer Central’s 100 Days of Silence campaign and the nation’s most comprehensive direct-to-door suppressor dealer, offers an installment payment program that allows buyers to spread the cost of their suppressor purchase over the ATF approval period. Buyers select their suppressor, make a down payment, and submit the Form 4 paperwork — then continue making installment payments while the ATF processes the application. When ATF approval is received and the suppressor is ready to ship, the balance is paid and the suppressor ships directly to the buyer’s door. Silencer Central handles all Form 4 preparation, CLEO notification, and NFA Gun Trust setup at no additional charge regardless of whether the buyer uses the installment program. Contact Silencer Central directly for current program terms, down payment requirements, and installment amounts for specific models, as financing programs are subject to change. Silencer Central’s national licensing in all 50 states means their payment program is available to buyers across the suppressor-legal states without requiring a local dealer.

Suppressor financing: Local Dealer Layaway and Payment Plans

Many local NFA dealers offer layaway or payment plans for suppressor purchases, particularly for buyers with established customer relationships. Under a typical layaway arrangement, the buyer makes a deposit and a series of scheduled payments until the suppressor’s purchase price is paid in full — at which point the Form 4 is submitted and the NFA transfer process begins. Layaway differs from a post-Form 4 payment plan in that the buyer typically must pay the full suppressor price before the transfer paperwork is submitted. Dealer payment plan terms vary widely — some dealers offer 0% interest plans for existing customers, while others use standard consumer financing with interest rates that may range from 6% to 25% annually depending on the financing partner and buyer credit profile. When evaluating a local dealer payment plan, ask about: total interest cost over the plan period, whether the Form 4 is submitted at purchase or after payoff, any fees for early payoff, and what happens to payments if ATF denies the Form 4 application.

Suppressor financing: Consumer Financing Through Credit Cards and Personal Loans

Standard consumer financing tools — credit cards, personal loans, and point-of-sale financing services — can be used for suppressor purchases with the same considerations as any other large discretionary purchase. A zero-percent introductory rate credit card used for a suppressor purchase and paid off within the promotional period is effectively free financing — the buyer spreads the cost over 12–18 months at no interest cost, which aligns well with the NFA processing timeline even in 2026’s improved environment. Personal loans through credit unions (often the best rates for members) or online lenders provide fixed payment schedules and potentially competitive rates compared to dealer financing. Point-of-sale financing services such as Affirm, Klarna, or dealer-specific programs may be accepted by some suppressor retailers for online purchases, though availability varies by dealer and state. For buyers with excellent credit, personal loans from credit unions or a no-interest credit card promo offer the most cost-effective financing across most scenarios.

Suppressor financing: The $0 Tax Stamp and What It Means for Financing in 2026

The elimination of the $200 federal tax stamp effective January 1, 2026, directly reduces the all-in cost of any suppressor purchase by $200, which meaningfully changes the financing math. A suppressor that previously required $800 total ($600 suppressor + $200 tax) now requires $600 total — a 25% reduction in acquisition cost. For buyers financing over 12 months, this means $17 lower monthly payments. More importantly, the $200 savings can be applied toward a higher-quality suppressor — the entry tier of suppressor quality that was previously budgeted at $400 ($200 suppressor + $200 tax) effectively becomes accessible at $400 for a suppressor alone. Combined with faster ATF approval times, the 2026 financing landscape represents the most accessible period in NFA history for first-time suppressor buyers who want to spread their purchase cost.

Suppressor financing: NFA-Specific Financing Considerations

Several characteristics of NFA purchases require specific attention when evaluating financing terms. Refund and return policies: most NFA dealers do not accept returns on suppressor purchases once the Form 4 has been submitted, because the registered item is associated with the specific buyer and transfer. Verify your dealer’s refund policy before purchase, and understand that financing a suppressor is generally a commitment to a specific item that cannot easily be returned or exchanged if your preference changes. ATF denial: in the rare case that an ATF Form 4 application is denied (due to a disqualifying background check result, incomplete paperwork, or other issue), the suppressor cannot transfer to the buyer. Most dealers will refund the suppressor purchase price in this case, but financing obligations — including accrued interest — may still be the buyer’s responsibility depending on the financing contract. Verify how the dealer and financing partner handle ATF denial scenarios before signing any financing agreement.

How to Evaluate Suppressor Financing Offers

When comparing financing options for a suppressor purchase, evaluate these key terms: annual percentage rate (APR) — the true cost of credit on an annualized basis, including all fees; total cost of financing — the total amount paid above the purchase price over the full financing term; prepayment provisions — whether you can pay off early without penalty (important if you want to pay down faster when the budget allows); Form 4 submission timing — does the dealer submit your Form 4 at purchase or only after full payoff; and deposit requirements. For buyers with good credit, the lowest-total-cost approach is typically a 0% promotional credit card paid within the promotional period. For buyers who prefer fixed monthly payments without credit card management, a dealer installment plan or personal loan from a credit union at competitive rates is the best structured option. Always read the complete financing agreement before signing, and confirm all verbal commitments about NFA-specific policies are documented in writing.

Suppressor financing: Budgeting Realistically for Your First Suppressor in 2026

A realistic first-suppressor budget in 2026 should account for the suppressor’s purchase price (typically $400–$600 for quality entry-level options, $600–$1,000 for mid-tier, $1,000–$1,500+ for premium), any dealer transfer or service fees, the NFA Gun Trust (free with Silencer Central purchases), and any accessories needed for your specific host (thread adapter if needed, thread protector, suppressor storage case). With the $200 tax stamp eliminated, first-time buyers who previously deferred over tax cost have clear entry points at every price tier. Silencer Central’s free NFA Gun Trust and included CLEO notification service eliminate what were historically additional costs for first-time buyers. Financing $500–$700 over 12 monthly payments at a range of interest rates produces monthly obligations of $45–$65 at 0% and $50–$75 at 12% APR — a manageable addition to most monthly budgets, particularly for buyers who can use the ATF wait period as a built-in savings runway.

Frequently Asked Questions About Suppressor Financing

Can I finance a suppressor while waiting for my Form 4 to be approved?

Yes. Most suppressor financing arrangements allow buyers to make installment payments during the ATF Form 4 processing period. Silencer Central’s payment program and many dealer layaway plans are specifically structured around the NFA wait time, allowing buyers to pay down their balance while ATF processes the application. In 2026, with Form 4 approvals processing in days rather than months for eForm 4 submissions, buyers using installment plans may find that approval arrives before they have made many payments — verify with your dealer how payment is handled if ATF approval comes earlier than the payment plan’s duration.

Is there a credit check for suppressor financing?

It depends on the financing method. Dealer layaway with only the dealer’s money does not typically require a credit check. Dealer-offered consumer financing through a bank or lending partner does typically require a credit check. Credit card purchases use the buyer’s existing credit limit and do not require a separate application for most buyers. Personal loans from a bank or credit union require a credit application. Silencer Central’s specific payment program terms — including whether a credit check is involved — should be confirmed directly with Silencer Central at the time of purchase inquiry, as program terms can evolve.

What happens to my financing if the ATF denies my Form 4?

ATF Form 4 denials are relatively rare but do occur, typically when a background check reveals a disqualifying condition. In a denial, the suppressor cannot transfer to you, and the dealer retains the item. Most dealers will refund the suppressor’s purchase price, minus any non-refundable fees. However, your financing obligation — particularly if you financed through a third-party lender (credit card, personal loan, point-of-sale financing) — may continue regardless of the ATF decision. The lender’s obligation is to you, not to the ATF process. Review your specific financing agreement’s terms regarding refunds and ATF denials, and verify in writing how the dealer handles this scenario, before committing to a financed purchase.

Disclosure: PopularSuppressors.com is operated by Brand Avalanche Media, Inc. This article contains general information about financing options for suppressor purchases. It is not financial or legal advice. Financing terms, availability, and conditions change frequently — verify all terms directly with Silencer Central or your dealer before making any purchase decision. Silencer Central is a paid sponsor of this website.

Similar Posts

Frequently Asked Questions

Can I finance a suppressor purchase?

Yes. Silencer Central offers the EZ Pay financing plan, which spreads the cost of your suppressor and $200 tax stamp into monthly payments. You can start your ATF Form 4 paperwork immediately while paying over time — your suppressor ships to your door once the ATF approves your application. Apply at SilencerCentral.com.

How much does a suppressor cost monthly on a payment plan?

Monthly payments depend on the suppressor price and term selected. A BANISH 30 Gold at approximately $999 plus the $200 tax stamp financed over 12 months through Silencer Central's EZ Pay runs roughly $100/month before interest. Exact payment terms are available at SilencerCentral.com.

Does financing affect how long it takes to get my suppressor?

No. Financing through Silencer Central's EZ Pay does not affect ATF processing times. Your Form 4 is submitted immediately after purchase, and the approval wait — currently 3–8 months via eForms — runs concurrently with your payment plan.